Future or Fantasy: The Real Economics of Yield Farming

In our latest market analysis piece, we discuss liquidity, value creation, and what the hell is going on in the magic land of yield farming. Let's dive in.

There is a lot of DeFi-specific lingo that one needs to learn to be able to lift the veil on DeFi. At the heart of it, the current craze is fueled by the advent of two types of tokens:

- Pool tokens

- Reward tokens

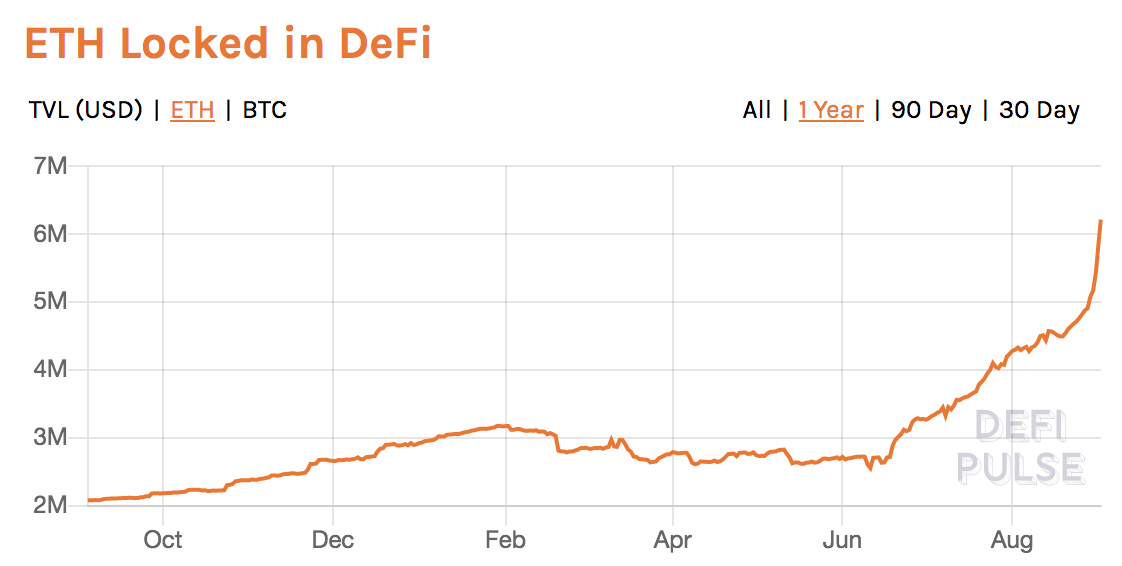

Pool tokens are responsible for a large majority of the explosion of DeFi’s Total Value Locked (a.k.a. TVL), a metric broadly seen as DeFi’s Open Interest. Reward tokens are responsible for the sky-high returns DeFi projects seem to generate.

How did these tokens manage to achieve both those things in just a couple of months? What are they used for? Do they really represent a new paradigm for DeFi? To answer these questions, let’s go back to a simpler time when Compound had about $100M being lent on any given day, Aave only a few million dollars, and Uniswap was breaking a mere $100k in daily trading volumes on good days.

cTokens or the ancestry of pool tokens

The first popular implementation of the concept of pool tokens dates from two years ago when the folks at Compound had a brilliant idea: they would tokenize the participation in any of Compound’s lending pools. This is how it worked:

- Alice owns 100 DAI.

- Alice notices the DAI lending pool on Compound is paying 12% APR.

- Alice deposits 100 DAI in the Compound DAI lending pool.

- Alice receives 100 cDAI, a pool token, against that deposit.

Now consider the relationship between DAI and cDAI. On the day of launch, cDAI/DAI = 1.00. However, after 1 month, cDAI/DAI = 1.01 (ignoring the compounding effect). And after 1 year, cDAI/DAI = 1.12. This works just like a zero-coupon bond, the price of which inexorably converges towards 100% as it gets closer to expiry. Similarly, buying cDAI instead of DAI allows an investor to earn Compound’s DAI interest rate without having to ever interact with Compound. But it had another effect that was less obvious at the time: it allowed DeFi to generate TVL out of thin air.

Indeed, assuming another protocol (let’s say Aave) would accept cDAI as deposit, and give Alice her own tokenized pool token (let’s say aDAI) in exchange for that deposit, then we would have Alice’s 100 DAI represented as 100 cDAI + 100 aDAI, i.e. a grand total of $200 worth of “value” locked. Any new protocol tends to accept all other protocols’ pool tokens, i.e. any new protocol has the potential to increase DeFi’s TVL by 100%. This simple realization goes a long way to explain this:

I know what you are thinking: potentially, DeFi’s TVL could increase 100% every time a new protocol launches, but this assumes participants pour all their pool tokens (no pun intended) into every new protocol that appears. That is clearly not a realistic scenario! Going back to our Aave example, Aave could launch a cDAI lending pool, but why would anyone borrow cDAI when DAI is much more liquid and useful? If there were no borrowers, then the interest rate would be zero percent, so lenders would have no incentive to deposit their cDAI with Aave. Unless there are other incentives to participating in a pool?

Enter Reward tokens.

Reward tokens, or DeFi’s take on airdrops

What are reward tokens, how do they work, and how are they related to Pool tokens?

The first popular implementation of a reward token was achieved by… you guessed it, Compound. Earlier this year, Compound announced it would go fully decentralized and let the community dictate the rules of its protocol. Which asset to add, what collateral would be required, what interest rates dynamics would look like: al of these questions would all be decided by the Compound community through a governance token: COMP. That COMP token would be airdropped to users depending on their participation in Compound’s different lending pools. The more assets one would contribute to a pool, the more COMP that user would be able to claim (for a deeper dive into this, check out this past Market Update) and the more voting power that user would gain.

The story really starts to get interesting when COMP is listed. COMP/USD shot up from $15 to $300 in the first days of listing, turning the Compound team into overnight millionaires. Of course, this success did not go unnoticed: one by one, the most prominent DeFi protocols announced their intention to launch their own governance (read: reward) token. The story is always more or less the same:

1. Lock your tokens in Protocol X, for example:

- Aave

- Compound

- Balancer

- Curv

- yearn.finance

- Uniswap

2. Receive pool token (a.k.a. LP tokens, or liquidity provider tokens) against that deposit:

- Aave: aTokens

- Compound : cTokens

- Balancer: BPT

- Curv: [pool name] Curve tokens

- Yearn.finance: yTokens

- Uniswap: UNI-V2-LP

3. Receive reward tokens (the more you deposit, the more reward tokens you earn):

- Aave: AAVE (not yet launched)

- Compound: COMP

- Balancer: BAL

- Curv: CRV

- Yearn.finance: YFI

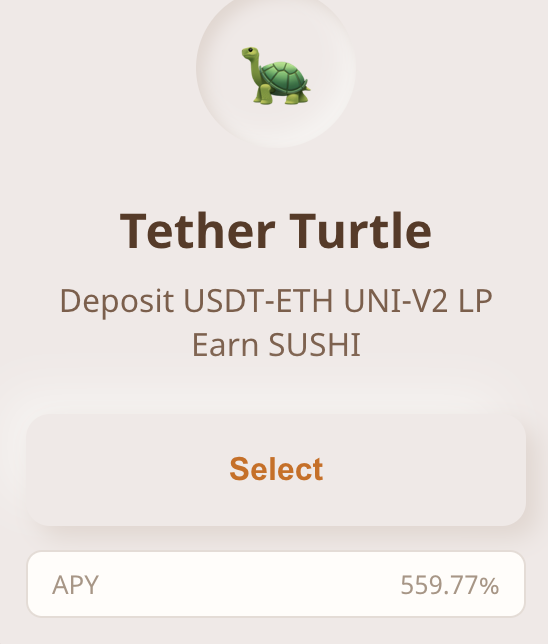

Keep in mind that most protocols accept other protocols’ pool tokens AND reward tokens as deposits to their own pools. For example, SushiSwap:

The annual percentage yield stated is obviously not driven by the fees this pool generates: most, if not all of it, is generated by the airdropping of SUSHI tokens paid in exchange for the locking of that Uniswap pool token.

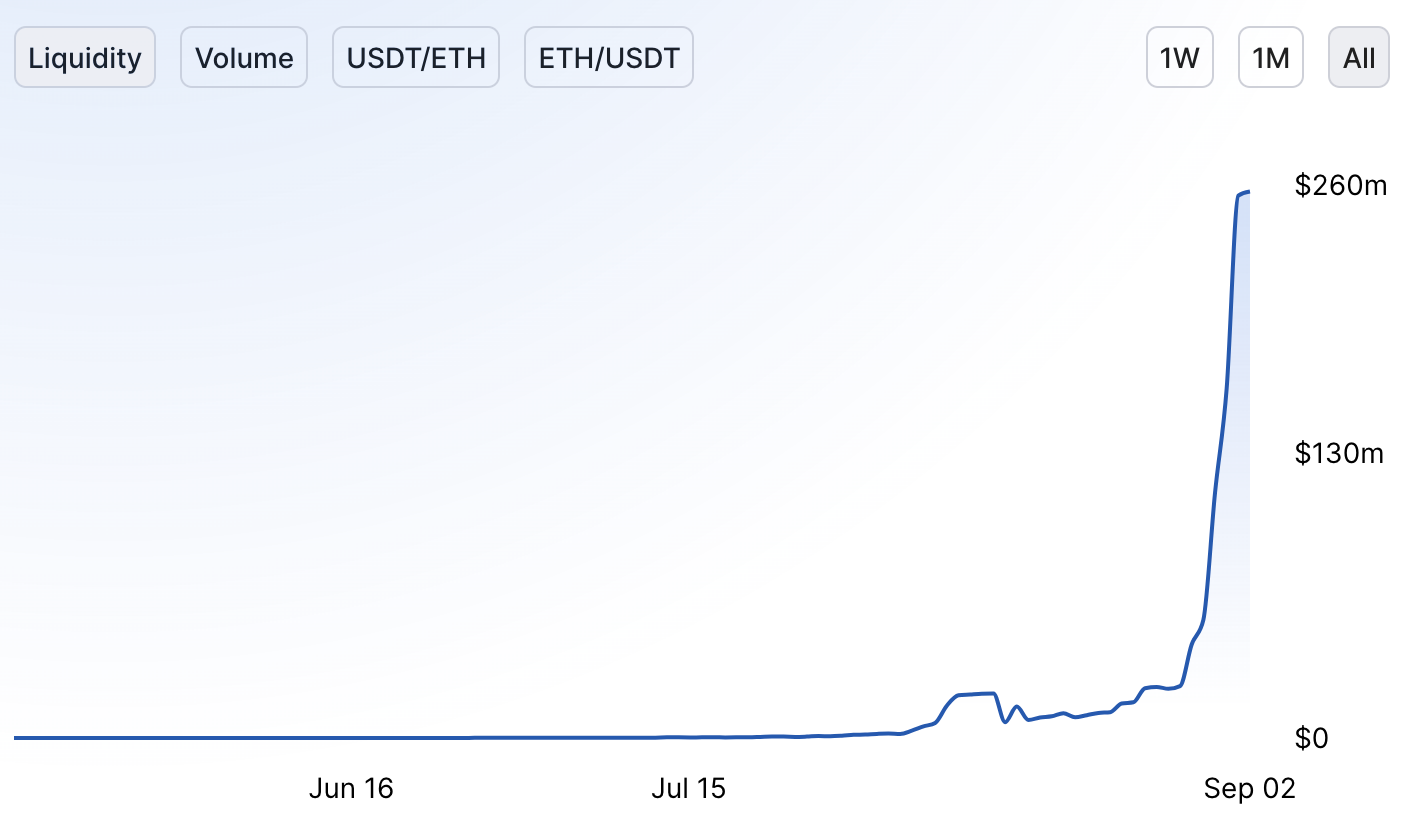

The effect on that Uniswap pool were immediate:

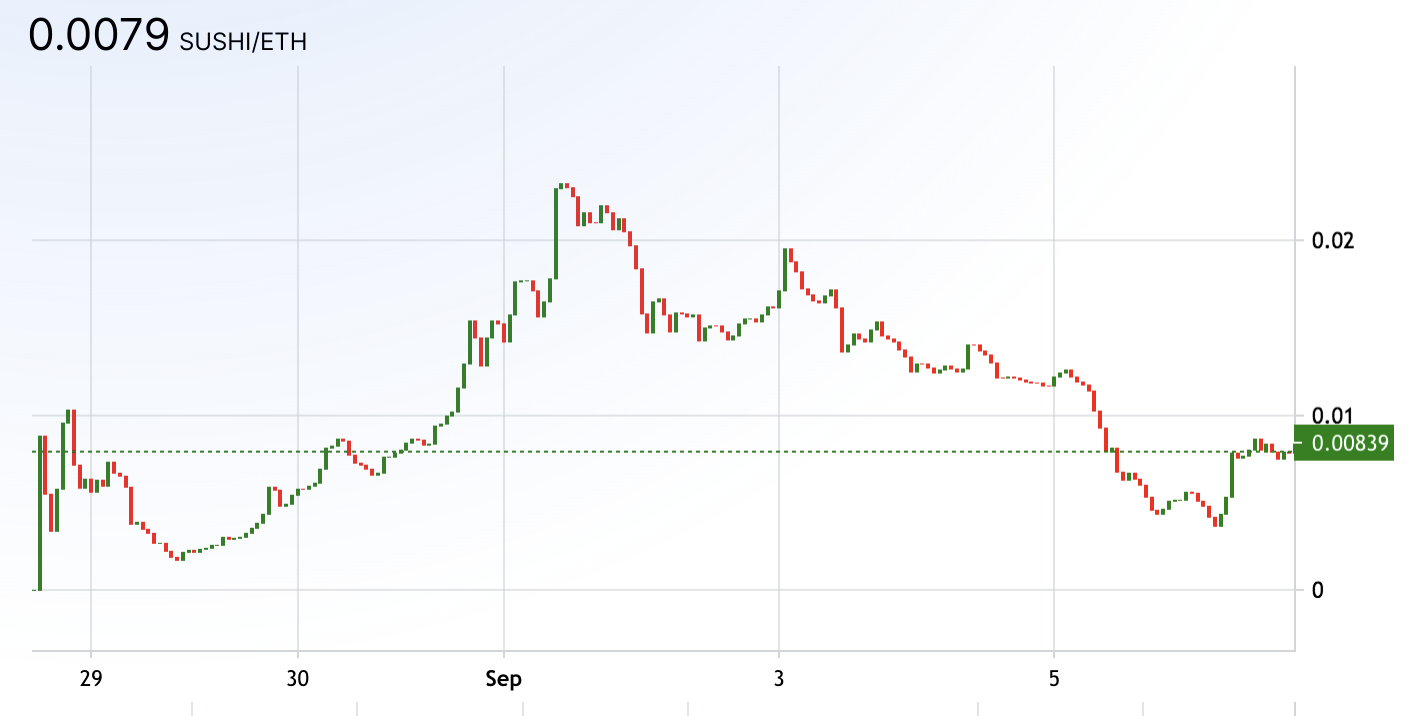

Uniswap ETH-USDT pool grew by 25x overnight as the herd of DeFi “farmers” tried to maximize their SUSHI airdrops. Why would they go after SUSHI, a two day-old token? Here comes the crux of this set-up: SUSHI will only attract depositors if its price is seen as attractive in the first place. Not a problem! Early holders of SUSHI can open a market (ie. pool) on Uniswap and determine its price by changing the amount of counter-currency they will deposit against it.

For example, if I am the first user to open a SUSHI-ETH pool and I deposit 1 SUSHI and 1 ETH, then 1 SUSHI = $430.

From there, it’s the all-too-common greed loop: price goes up, I should buy more, so price goes up...

As I write these lines, new protocols are popping up daily, and why shouldn’t they? Open-source means anyone can copy an existing protocol, stick a new catchy name on it and hope to get noticed.

Is this sustainable? DeFi is undeniably growing, but its newly found attractivity is not based upon innovative use cases or reaching vast numbers of unbanked users. Instead, it is supported by the constant airdrop of tokens, the core value of which—governance—is hard to measure, hence it is prone to mania. Finally, we have glanced over the risks attached to participating in such pools, but those risks are very real, and often happily ignored. We will do a deeper dive into that subject in the next Market Update, so stay tuned.

Legal Disclaimer

This e-mail is being distributed by CoinList Lend, LLC, a subsidiary of Amalgamated Token Services Inc. (together with its subsidiaries, “CoinList”). All hypotheses, opinions and theories are those of the author and do not necessarily reflect the views or positions of CoinList. Nothing in this e-mail shall constitute or be construed as an offering of securities or as investment advice or investment recommendations (i.e., recommendations as to whether to enter or not to enter into any transaction involving any specific interest or interests) by CoinList or any of its affiliates or a recommendation as to an investment or other strategy. These types of investments involve a high degree of risk (including risk of total loss) and potential investors should consult with their own advisors. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions or future events or performance are not statements of historical facts and may be “forward looking statements.” Forward looking statements are based on expectations, estimates and projections at the time the statements are made that involve a number of risks and uncertainties which could cause actual results or events to differ materially from those presently anticipated.

CoinList is not a bank or investment advisor and does not provide any such services, nor does it offer legal or tax advice. Virtual currency is not legal tender, is not backed by the government, and accounts and value balances are not subject to Federal Deposit Insurance Corporation or Securities Investor Protection Corporation protections.

Certain services may be limited to residents of certain jurisdictions, and certain disclosures are required in certain jurisdictions, available here.

This e-mail contains references to information obtained from third-party content providers (content hosted on sites unaffiliated with CoinList). As such, CoinList makes no representations whatsoever regarding any information obtained from third parties that may be referenced directly or indirectly in this e-mail.

The information in this email, including any indicative rates or fees, is subject to change at any time. Use of the CoinList website is subject to certain risks, including but not limited to those listed here.